- Opportunity Zone funds are tax-deferral tools, not risk-free tax shelters. The investment still has to make economic sense after fees, leverage, liquidity limits, and execution risk.

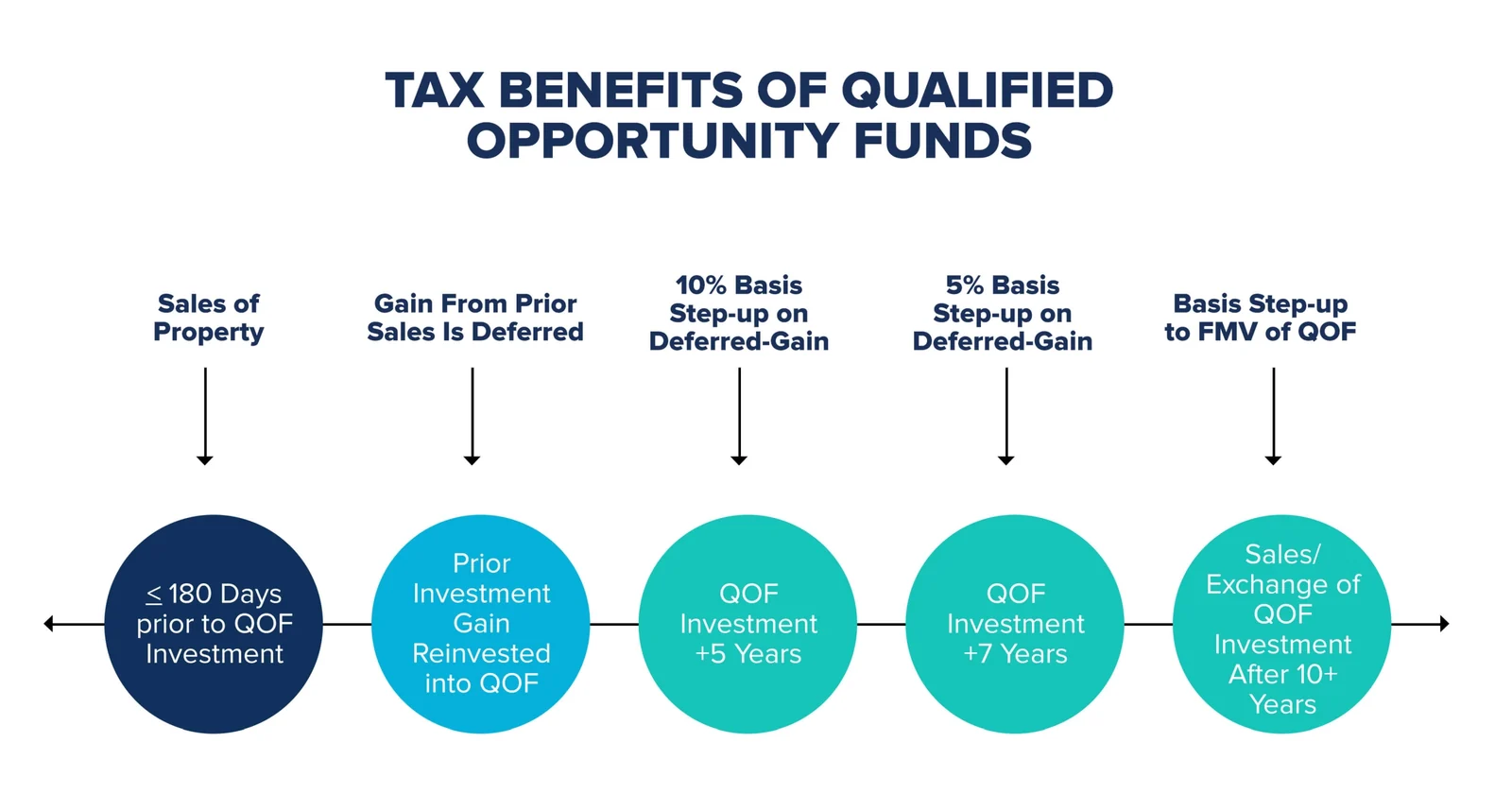

- Investors generally have 180 days from the gain-recognition date to invest eligible capital gains into a Qualified Opportunity Fund.

- The biggest potential benefit comes from the 10-year holding period: qualifying investors may be able to exclude appreciation on the Opportunity Zone investment itself.

- The original program’s deferred-gain inclusion date is December 31, 2026; newer Opportunity Zone rules and rural enhancements continue to evolve under recent legislation and IRS guidance.

- Before investing, review fund quality, project-level risk, cash-flow expectations, exit strategy, state-tax treatment, and whether the allocation fits your broader financial plan.

A large capital gain can create a good problem: a business sale, real estate sale, concentrated stock position, or private-company liquidity event may leave you with new flexibility — and a tax bill that arrives quickly. Qualified Opportunity Funds, often called Opportunity Zone funds or QOFs, were designed to encourage long-term investment in designated communities while giving investors a way to defer eligible capital gains.

For high-net-worth families and business owners, the idea sounds attractive: sell an appreciated asset, reinvest the gain, defer tax, and potentially eliminate tax on the new investment’s appreciation after a long holding period. But the strategy is only as good as the underlying investment. The tax benefit should be the final enhancement, not the reason to ignore risk.

How Opportunity Zone Funds Work

A Qualified Opportunity Fund is generally a partnership or corporation formed to invest in Qualified Opportunity Zone property. The fund must satisfy IRS rules, including a requirement that a high percentage of its assets be invested in qualifying Opportunity Zone property. Investors do not usually buy the property directly; they buy an interest in the fund.

The basic planning sequence looks like this:

- Realize an eligible capital gain. This might come from selling a business, real estate, public stock, private stock, or another appreciated capital asset.

- Invest the gain into a Qualified Opportunity Fund. The IRS generally gives investors 180 days from the date the gain would otherwise be recognized to invest the eligible gain.

- Elect deferral on the tax return. The taxpayer must make the proper election and maintain documentation. This is a tax-reporting matter that should be coordinated with a CPA.

- Hold for the intended time horizon. The longer the qualifying QOF investment is held, the more valuable the potential tax benefits become.

The Three Tax Benefits Investors Care About

| Benefit | What It Means | Planning Point |

|---|---|---|

| Deferral | Eligible capital gains invested in a QOF can be deferred instead of recognized immediately. | For the original Opportunity Zone program, remaining deferred gain is generally included no later than December 31, 2026, or earlier if there is an inclusion event. |

| Potential basis step-up | Some rules provide basis increases after meeting specified holding periods. | Step-up rules depend on the investment date and governing law. Investors should confirm the applicable rule set before relying on it. |

| 10-year appreciation exclusion | If a qualifying QOF investment is held for at least 10 years, investors may be able to elect to step up basis to fair market value on sale. | This is often the most meaningful benefit, but it requires patience and a successful underlying investment. |

Opportunity Zone planning is most compelling when the fund is attractive even without the tax benefit. If the economics only work because of the tax deferral, the investor may be taking too much risk for a timing benefit.

What Changed Under Recent Opportunity Zone Legislation

The Opportunity Zone program has been modified since its original creation under the 2017 Tax Cuts and Jobs Act. Recent federal legislation made the program more durable and introduced rural-area enhancements. IRS materials describe a rural-area definition and note that, beginning July 4, 2025, the substantial-improvement threshold for certain property located entirely in rural Qualified Opportunity Zones was reduced from 100% to 50%.

For investors, the practical takeaway is not to assume every Opportunity Zone fund follows the same rule set. Legacy investments, new investments, rural-focused funds, and future-designated zones may have different compliance requirements, time horizons, and tax outcomes. This is an area where fund documents, tax counsel, and CPA review matter.

Who Might Be a Fit?

Opportunity Zone funds are usually most relevant for investors who have a meaningful realized capital gain and can commit capital for a long period. They may come up after:

- a business sale or partial liquidity event,

- a sale of highly appreciated real estate,

- diversification out of concentrated public stock,

- private-company stock liquidity, or

- large taxable portfolio rebalancing.

They are usually a poor fit for investors who need near-term cash, dislike K-1 complexity, cannot tolerate private investment risk, or are trying to use tax savings to justify an investment they would otherwise avoid.

Due Diligence Before Investing

Investors should underwrite both sides of the decision: the tax structure and the investment itself. A thoughtful review should include:

- Fund strategy: Is the fund building ground-up real estate, improving existing property, financing operating businesses, or using leverage?

- Manager quality: What is the manager’s track record through full market cycles, not just projections?

- Fees and promotes: How much return must the project generate before the investor benefits?

- Cash-flow expectations: Will the fund distribute cash, or is most of the return expected at sale?

- Exit planning: How realistic is the 10-year exit path, and who controls the timing?

- Tax reporting: What K-1 timing and state-tax complexity should you expect?

- Portfolio fit: Does the allocation create overexposure to real estate, development risk, or one geography?

A Simple Planning Example

Assume a business owner sells appreciated stock and realizes a $1,000,000 long-term capital gain. Instead of paying the full federal capital-gains tax immediately, the owner invests the gain into a Qualified Opportunity Fund within the required window and makes the proper election. The original gain is deferred under the applicable rules. If the QOF investment is held for at least 10 years and qualifies, appreciation inside the fund may be eligible for exclusion when sold.

That sounds powerful, but the result still depends on the fund. A strong project can make the tax benefit valuable. A weak project can turn deferral into a distraction. The right question is not “How much tax can I delay?” It is “Would I want to own this investment for a decade, and does the tax treatment improve an already sound plan?”

How We Think About Opportunity Zones for Reno Families and Business Owners

At GK Wealth Management, Opportunity Zone funds typically enter the conversation as part of a broader capital-gains plan. We look at the timing of the sale, existing portfolio risk, liquidity needs, charitable strategies, installment-sale alternatives, tax-loss harvesting, and the family’s long-term cash-flow goals before narrowing to a specific fund.

For the right investor, a QOF can be one tool among several. For the wrong investor, it can introduce illiquidity, complexity, and concentration at precisely the time a liquidity event should create flexibility. The planning work is separating those two situations before capital is committed.

Frequently Asked Questions

Do Opportunity Zone funds eliminate all tax?

No. They may defer eligible capital gains and may exclude appreciation on the QOF investment after a qualifying long-term hold. The original deferred gain is not automatically eliminated.

Can I invest only the gain, or do I have to reinvest the full sale proceeds?

The Opportunity Zone deferral generally applies to eligible capital gain. That means an investor may be able to reinvest only the gain amount rather than the entire sale proceeds, depending on the transaction and eligibility.

Are Opportunity Zone funds liquid?

Usually no. Many QOFs are private investments with multi-year lockups, limited secondary markets, and manager-controlled exit timing. Investors should assume the capital may be unavailable for a long period.

Should I use an Opportunity Zone fund after selling a business?

Maybe. A business sale is one of the situations where QOF planning may be worth evaluating, but it should be compared against cash needs, diversification, charitable planning, installment structures, state taxes, estate planning, and the quality of the specific fund.

Important disclosure: This article is for educational purposes only and should not be treated as individualized tax, legal, or investment advice. Opportunity Zone rules are complex and continue to be shaped by legislation, IRS guidance, fund structure, and individual facts. Consult your CPA, tax attorney, and financial advisor before making any investment or tax election. Investing involves risk, including possible loss of principal. Private investments may be illiquid and are not suitable for all investors.