- Artificial intelligence is moving through cloud infrastructure, semiconductors, software, advertising, cybersecurity, healthcare, industrial automation, and power markets.

- A transformational technology can create enormous value and still produce a bubble in the wrong parts of the market.

- The central question is not whether AI is real. It is how much future success is already priced in.

- Disciplined investors should separate infrastructure winners, AI adopters, and AI tag-alongs before deciding what they actually own.

Artificial intelligence is not a niche story anymore. It is moving through cloud infrastructure, semiconductors, software, advertising, cybersecurity, healthcare, industrial automation, and even power markets.

That does not automatically make every AI stock a good investment. A transformational technology can create enormous value — and still produce a bubble in the wrong parts of the market.

The Number That Changes the Conversation

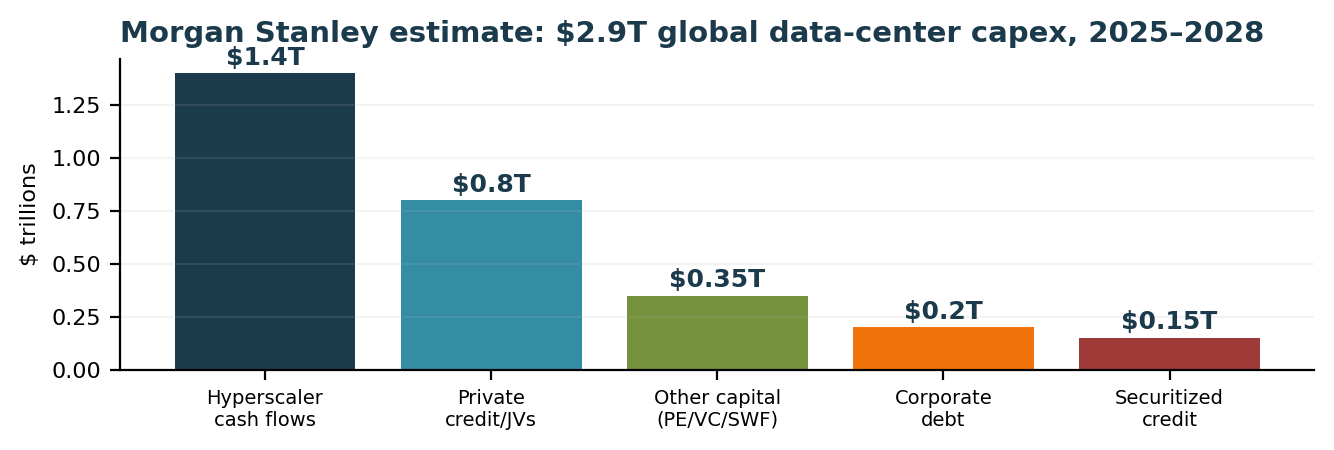

Estimated global data-center capex, 2025–2028. Source: Morgan Stanley Research.

| Indicator | What It Shows | Source |

|---|---|---|

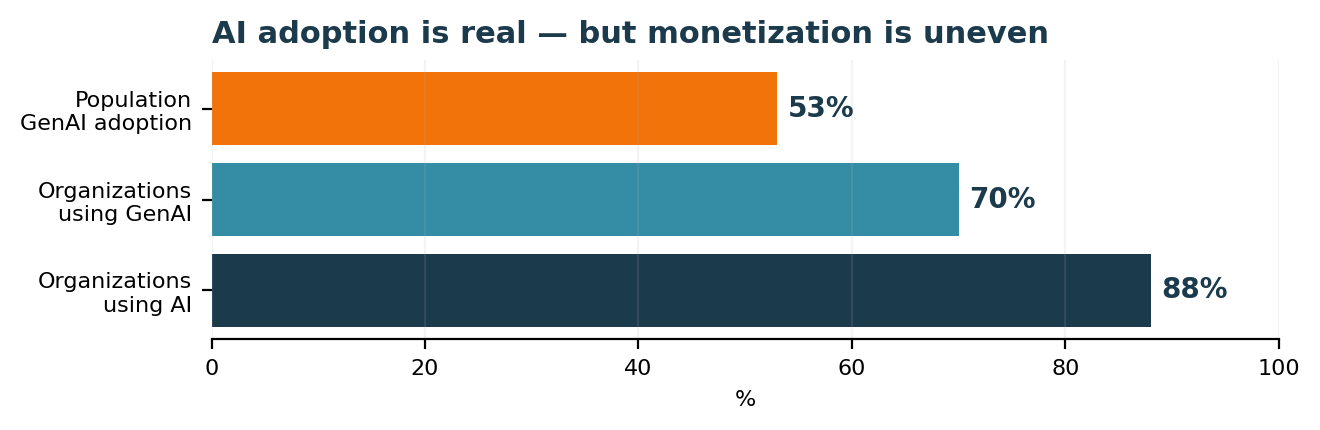

| 88% | Organizations reporting AI use in at least one function. | Stanford AI Index / McKinsey |

| 53% | Population-level GenAI adoption within 3 years. | Stanford AI Index 2026 |

| $2.9T | Estimated global data-center capex from 2025–2028. | Morgan Stanley Research |

Those numbers are why AI deserves attention. Adoption is broad, infrastructure spending is massive, and consumers are using the tools faster than prior major computing waves.

But big numbers cut both ways. When capital floods into one theme, prices often start assuming perfection.

Theme vs. Bubble: Both Can Be True

| What Looks Real | What Can Still Go Wrong |

|---|---|

| AI adoption is spreading across companies and consumers. | Adoption does not guarantee profits for every AI-linked company. |

| Cloud, chips, power, and data centers have visible demand. | Capex can overshoot if future usage, pricing, or returns disappoint. |

| Productivity gains may lift margins for strong adopters. | Investors may overpay before the productivity shows up in earnings. |

| The best platforms may compound for years. | The “AI label” can inflate weak businesses with little durable edge. |

Sources: Stanford HAI 2026 AI Index; McKinsey State of AI surveys. Figures are broad adoption indicators, not portfolio recommendations.

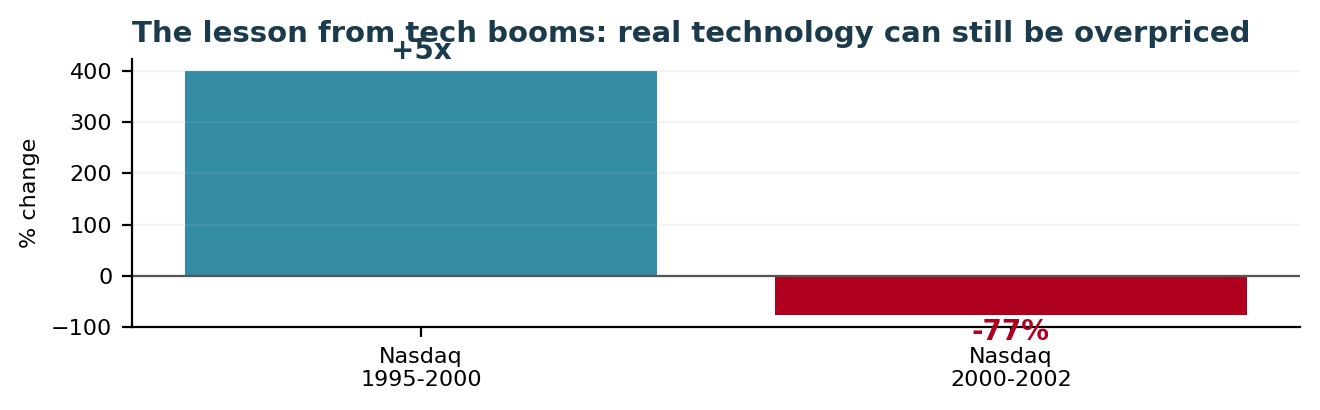

The Dot-Com Parallel

The internet changed the world. That did not prevent the Nasdaq from falling roughly 77% from its 2000 peak to its 2002 trough. The technology was real; the prices were the problem.

Sources: Goldman Sachs history of the dot-com bubble; Investopedia summary of Nasdaq 1995–2002 performance.

| Boom | What Was Real | What Became Dangerous |

|---|---|---|

| Nifty Fifty | Great companies, national brands | “One-decision” stocks priced as if growth never slowed |

| Dot-com | Internet adoption, e-commerce, connectivity | Revenue-free companies valued on page views and narratives |

| Housing / credit | Real demand for homes and credit | Leverage, weak underwriting, and belief prices could not fall |

| AI today | Real usage, real capex, real revenue for leaders | Crowded positioning, circular spending, and extreme future assumptions |

The Three AI Buckets Investors Must Separate

| Bucket | What It Means | Investor Question |

|---|---|---|

| 1. Infrastructure winners | Chips, cloud, data centers, networking, power, cooling. | Is demand durable after the first buildout wave? |

| 2. AI adopters | Companies using AI to cut costs, improve speed, or grow revenue. | Will AI improve margins or returns on capital? |

| 3. AI tag-alongs | Companies using AI language without clear economic benefit. | Is this a business model — or a marketing label? |

The Capex Boom Is the Opportunity — and the Risk

AI requires a physical buildout: chips, servers, land, data centers, transmission, water, power, and cooling. That creates investment opportunities beyond software. It also creates the classic boom-cycle risk: too much capital chasing too few proven returns.

Source: Morgan Stanley Research estimate cited in “AI Market Trends 2026.”

| Valuation Risk | Why It Matters |

|---|---|

| Growth already priced in | If a stock assumes years of flawless AI growth, a “good” result may not be good enough. |

| Capex payback uncertainty | Data-center spending must eventually convert into high-return cash flows. |

| Customer concentration | A few hyperscalers can drive a large share of AI infrastructure demand. |

| Index concentration | Investors may own more AI exposure than they realize through broad-market funds. |

| Narrative risk | When a theme is loved, disappointment can compress multiples quickly. |

What We Would Rather Own

| Prefer | Be Careful With |

|---|---|

| Cash-flow businesses with pricing power | Companies valued mainly on AI headlines |

| Firms with clear unit economics | Businesses spending aggressively without visible returns |

| AI adopters improving margins today | Stories that require perfect adoption years from now |

| Diversified exposure across the AI value chain | One-stock, one-sector, or one-theme concentration |

| Valuation discipline and position sizing | “It can only go up” thinking |

How Discipline Helps Capture the Theme

AI may be a multi-decade investment theme. That is exactly why investors should not treat it like a lottery ticket.

- Separate real earnings from future promises.

- Own exposure across beneficiaries — not only the most obvious names.

- Size positions so a valuation reset does not derail the plan.

- Rebalance when enthusiasm turns into concentration.

- Demand a margin of safety, even in great businesses.

The Bottom Line

The goal is not to avoid AI. The goal is to participate without becoming dependent on one theme being priced perfectly forever.

One Question to Ask Yourself Today

Am I investing in AI — or am I simply buying the crowd?

If the answer is the crowd, be careful. Crowds can push prices higher in the short term. Discipline protects capital over the long term.

Schedule a Portfolio Review →At GK Wealth Management, we want portfolios to participate in innovation while still being built for valuation risk, downside risk, and multiple market outcomes.

— Teddy Bakhos, CIO | GK Wealth Management